Sticking since 1988: Hindustan Adhesives

Sticking since 1988: Hindustan Adhesives

#Stock Discussion

As promised, I am starting the year by dipping into uncharted territory again. And in this post, we will discuss a company that is a bit sticky.

But before I begin, let me reiterate that the microcap segment of stocks is highly volatile in nature and you should exercise your judgment to invest in them only with surplus money, there are chances of permanent capital loss in them.

And I know you don’t like to read the annual reports, so let’s do it my way.

What does it do?

The company provides adhesive solutions for packaging, vertically integrated to offer an entire value chain of adhesive solutions from poly films, tapes, and packaging boxes.

Products: packaging tapes, tear tapes, polyolefin shrink films

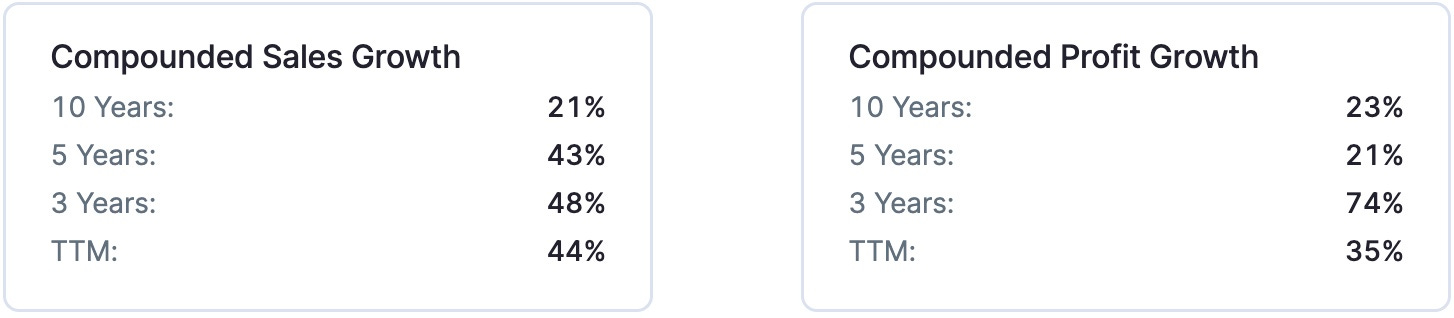

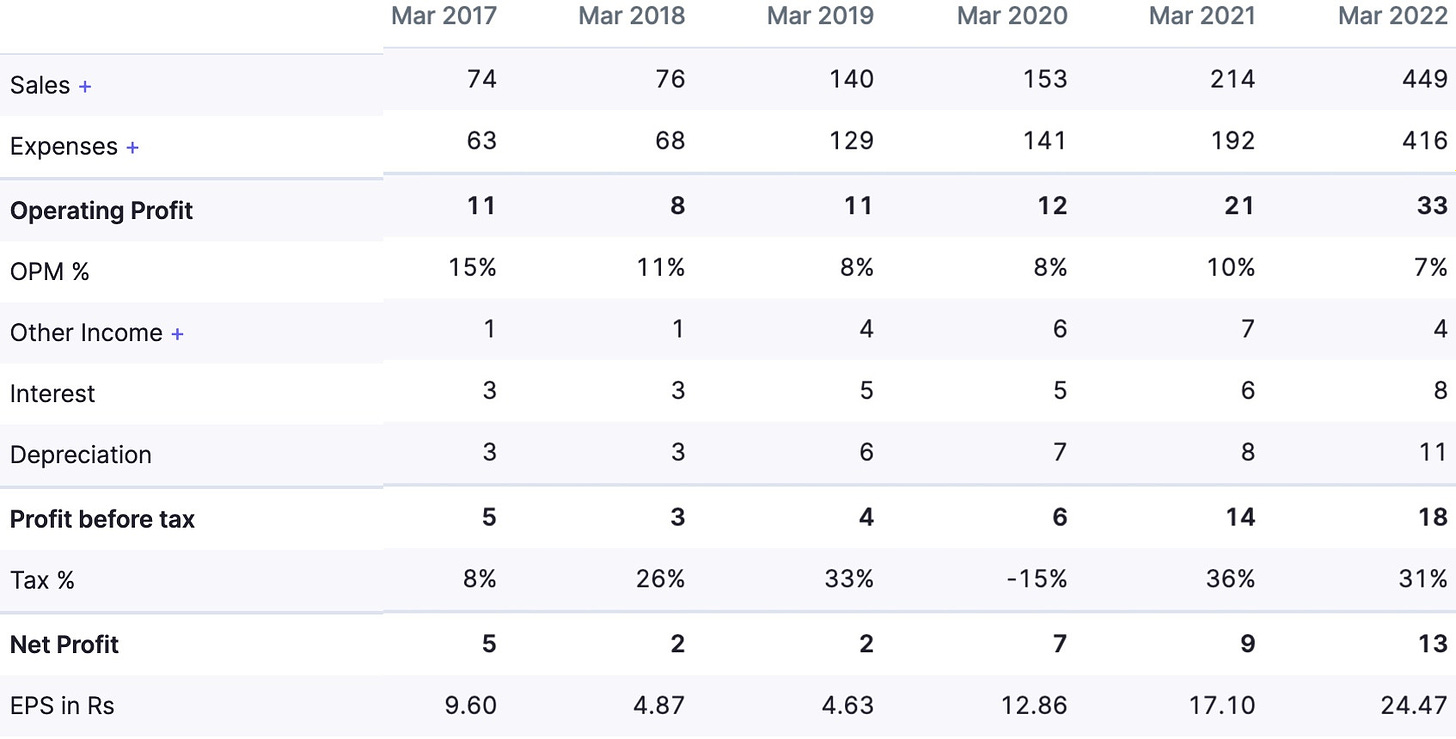

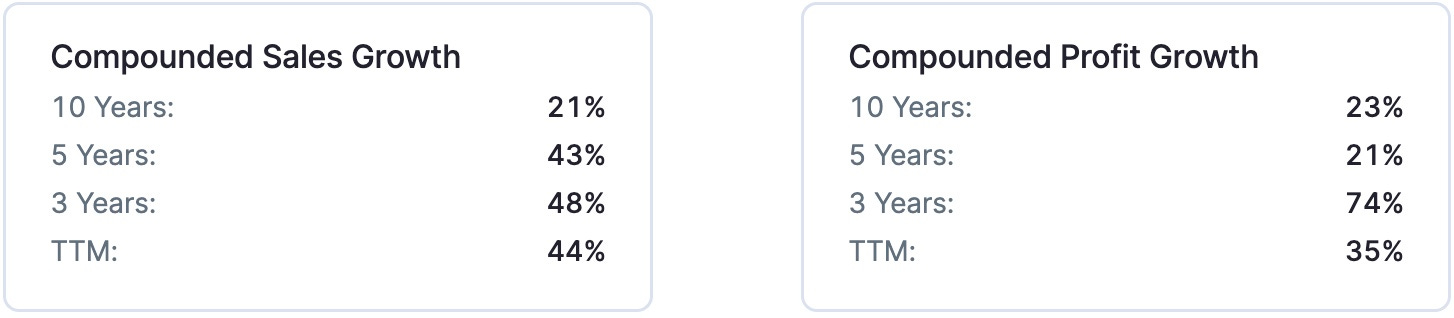

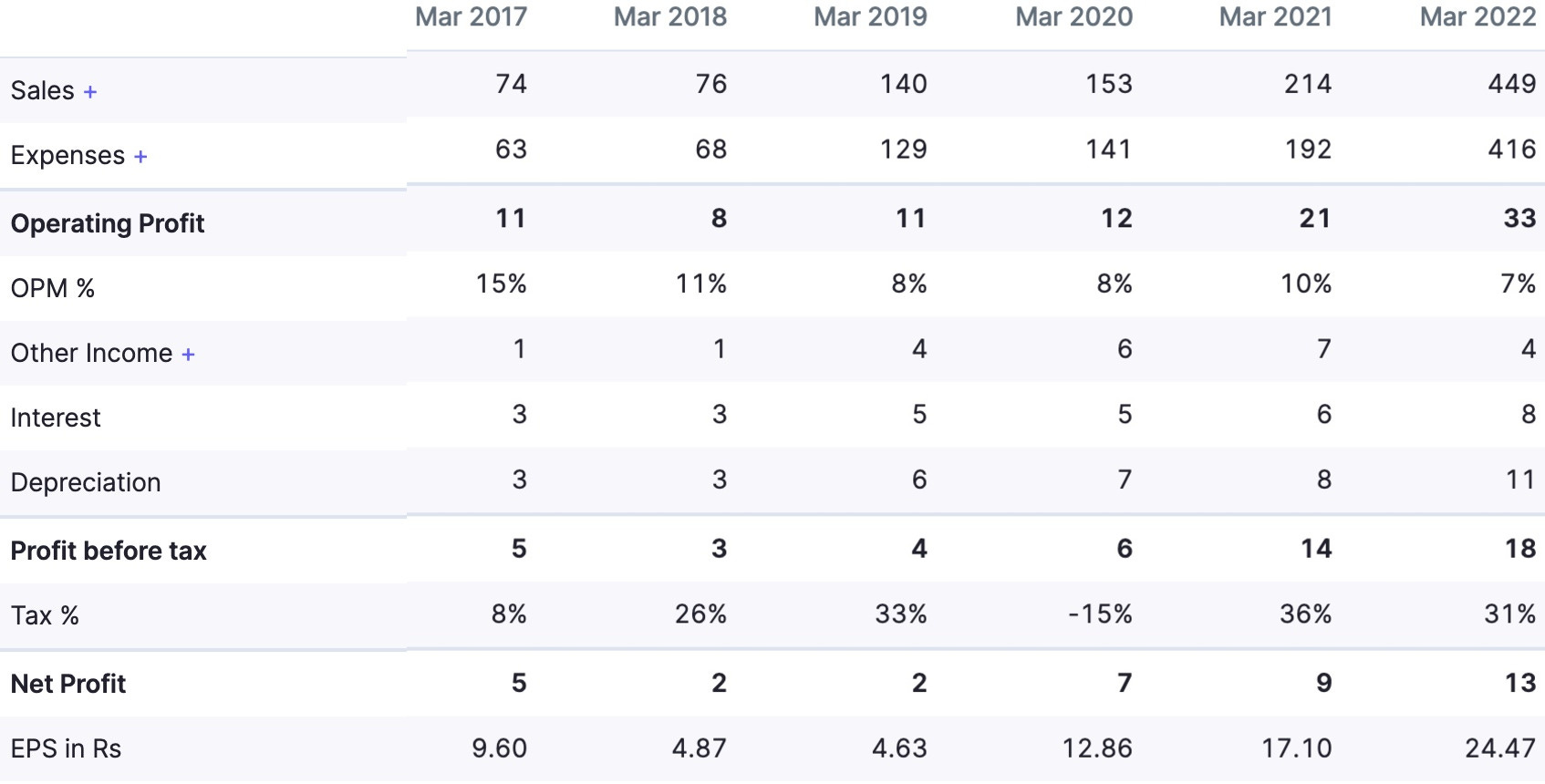

Sales and Profit growth - Phenomenal

Last 5 years’ performance

Notice moderate growth in 2020 and a bump up in 2022 (due to pent-up demand), also the shrink in margin from 15% to 7%

The margin shrink is mainly due to an increase in cost. Also, the material cost increased from 51% to 71% from 2017 to 2022.

Pledging - ZERO

Debt - 82 cr (Debt is very high due to recent CAPEX plans and micro-caps have no other way to raise capital, also half of these debts are short-term borrowing, and the interest is on the higher side. A close watch is necessary here.)

Dividend - No dividend paid (Don’t expect the debt-laden company to pay dividends but cashflow should be monitored, there is also a sudden increase in trade receivables, )

What’s the trigger?

The standardization of FMCG products, more products in the formal economy, and the launch of new products by clients, it’s packaging and overall consumption theme.

Quality of clients: Good enough to sustain for long term

Expansion: The Co expanded its capacity from 27.2 million sq. mt. to 42 million sq. mt. during FY21 by incurring a CAPEX of 30 crores primarily funded by debt.

Increased focus on overseas clients can be a good long-term trigger, the export has raised from 62% (in 2020) to 74% (in 2021).

Risk?

The obvious risk of investing in micro-cap stocks is loss of capital and the economic downturn risk which is not in our control. There is another risk of these stocks as they tend to be highly volatile.

The five-year chart for Hindustan adhesives looks like this.

There was a huge run-up in stock from 2021 to 2022 but since then it has corrected by more than 60%. So getting stuck on a higher price is a real risk in this stock.

And since the liquidity (number of shares available for selling/buying) are just about 50 lakhs with 68% of them lying with promoters, stock can behave highly volatile during optimism/trouble.

Having said that, another thing that I noticed in the micro-cap segment is the flow of information, unlike popular stocks, the information available in this area is very less. So keeping a regular watch on this stock is needed here.